Student Loan Forgiveness 2026: Federal Programs & Application Guide

The landscape of higher education finance is constantly evolving, and for millions of Americans, student loan debt remains a significant burden. As we look towards 2026, the discussion around student loan forgiveness 2026 continues to be a central topic for borrowers, policymakers, and financial experts alike. The prospect of debt relief, potentially exceeding $10,000 for many, offers a beacon of hope for those navigating the complexities of federal student aid programs. This comprehensive guide aims to shed light on the latest updates, provide clarity on existing and potential new programs, and offer actionable advice on how to position yourself to benefit from any forthcoming relief.

Understanding the intricacies of student loan forgiveness is crucial. It’s not a one-size-fits-all solution, and eligibility often depends on a myriad of factors, including loan type, employment history, income level, and specific life circumstances. Our goal is to demystify these processes, equipping you with the knowledge needed to make informed decisions about your financial future.

The Current State of Student Loan Forgiveness: What’s Available Now?

Before diving into future possibilities, it’s essential to understand the current federal student loan forgiveness programs that are active and available. These programs form the foundation upon which any new initiatives might be built or modified. Familiarizing yourself with these options is the first step in assessing your eligibility for any form of debt relief, whether it’s today or in 2026.

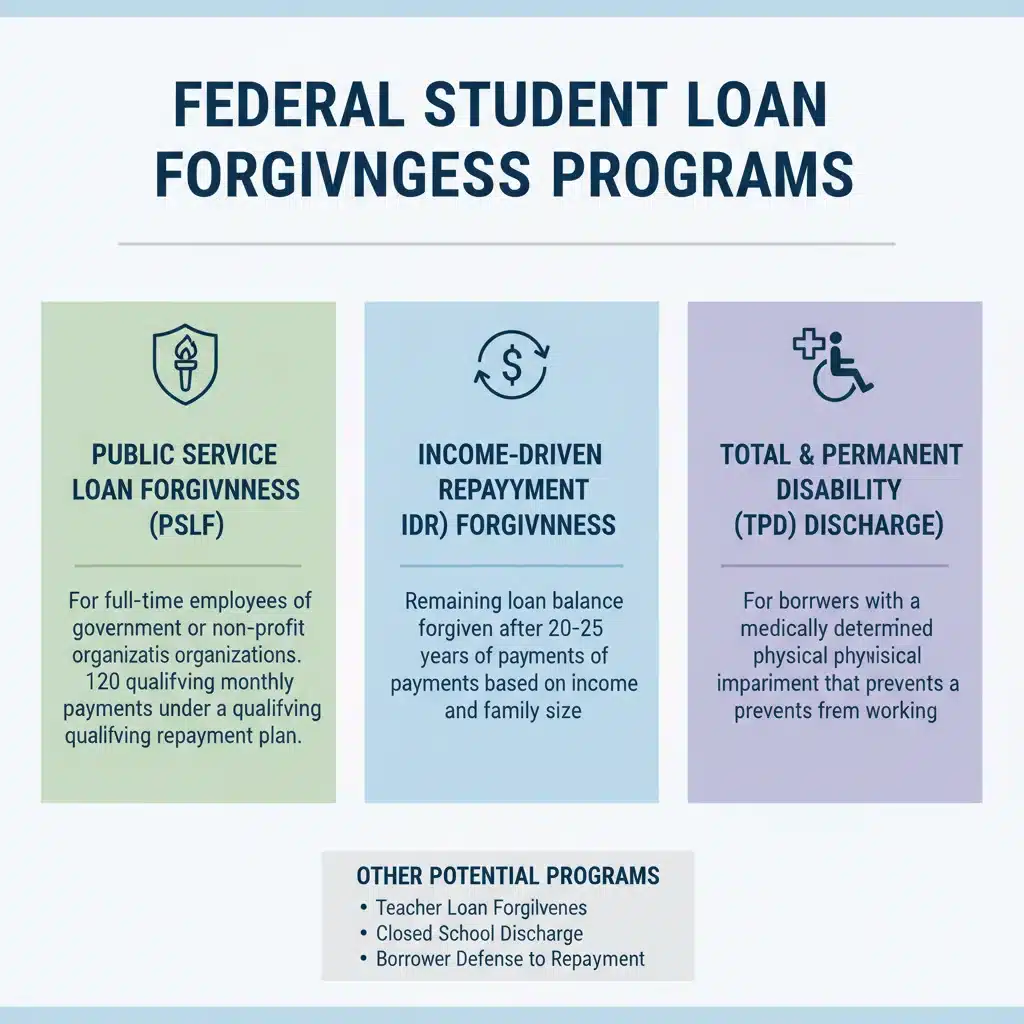

Public Service Loan Forgiveness (PSLF)

The Public Service Loan Forgiveness (PSLF) program is designed to forgive the remaining balance on Direct Loans for borrowers who work full-time for a qualifying non-profit organization or government agency. To qualify, you must make 120 qualifying monthly payments under a qualifying repayment plan. This program has seen significant attention and some reforms in recent years, making it more accessible to eligible public servants. Keeping track of your employment and payments is paramount for PSLF.

Income-Driven Repayment (IDR) Plan Forgiveness

Income-Driven Repayment (IDR) plans offer a pathway to forgiveness after a certain number of years of payments (typically 20 or 25 years, depending on the plan and whether you have graduate school loans). These plans adjust your monthly payment based on your income and family size, making payments more affordable. Any remaining balance after the required payment period is forgiven, though it may be subject to income tax. The recent SAVE Plan (Saving on a Valuable Education) is the newest IDR plan, offering even more generous terms for many borrowers, including lower monthly payments and a faster path to forgiveness for some.

Teacher Loan Forgiveness

Teachers who work for five complete and consecutive academic years in low-income schools or educational service agencies may be eligible for up to $17,500 in loan forgiveness. The specific amount depends on the subject taught. This program is distinct from PSLF, and borrowers cannot receive benefits from both for the same period of service.

Total and Permanent Disability (TPD) Discharge

Borrowers who are determined to be totally and permanently disabled can have their federal student loans discharged. This can be based on documentation from the Department of Veterans Affairs, the Social Security Administration, or a physician. The TPD discharge provides significant relief for those unable to work due to their disability.

Borrower Defense to Repayment

This program allows for the discharge of federal student loans if a school misled you or engaged in other misconduct in violation of certain state laws. This has been a significant area of focus, particularly for students who attended now-defunct for-profit colleges. The process for applying and receiving relief under Borrower Defense has been subject to various changes and legal challenges.

Closed School Discharge

If your school closed while you were enrolled or shortly after you withdrew, you might be eligible for a closed school discharge, which forgives 100% of your federal student loans obtained to attend that school. This applies if you couldn’t complete your program because of the closure and didn’t transfer your credits to another school.

Anticipating Student Loan Forgiveness 2026: What Could Change?

While the existing programs provide avenues for relief, the conversation around student loan forgiveness 2026 often centers on broader, more universal forms of debt cancellation. The political and economic climate plays a significant role in shaping these discussions. While no specific universal forgiveness plan is guaranteed for 2026, several factors suggest that student loan debt relief will remain a priority.

Political Landscape and Policy Initiatives

The federal government has demonstrated a willingness to address student loan debt through executive actions and legislative proposals. Future elections and changes in congressional control could lead to new initiatives. Discussions often revolve around:

- Broad-Based Forgiveness: Proposals for widespread student loan cancellation, often with caps (e.g., $10,000, $20,000, or more per borrower), are frequently debated. The rationale behind such proposals includes stimulating the economy, reducing racial wealth gaps, and providing relief to struggling households.

- Targeted Forgiveness Expansion: Instead of universal forgiveness, there might be expansions of existing targeted programs. This could mean making PSLF more accessible, simplifying IDR plan enrollment, or increasing the amount of forgiveness available through specific programs for certain professions or demographics.

- Simplification of Application Processes: A common critique of current forgiveness programs is their complexity. Future reforms could focus on streamlining application processes and improving communication to ensure eligible borrowers can more easily access relief.

Economic Considerations

The economy’s health significantly impacts the discussion around student loan forgiveness. High inflation, potential recessions, and the ongoing recovery from global economic disruptions can influence policymakers’ decisions. Debt relief is often seen as a tool to stimulate consumer spending and reduce financial stress on households, which could be a driving force behind new initiatives in 2026.

Department of Education Actions

Beyond legislative action, the Department of Education has considerable authority to implement changes to federal student loan programs. This includes refining IDR plans, adjusting eligibility for existing forgiveness programs, and even initiating new forms of relief through regulatory changes. These administrative actions can have a profound impact on millions of borrowers without requiring congressional approval.

Eligibility for Student Loan Forgiveness 2026: What to Prepare For

Regardless of whether new programs emerge or existing ones are expanded, certain foundational elements of eligibility are likely to remain consistent. Preparing for these now can put you in a better position to apply for student loan forgiveness 2026.

Federal vs. Private Loans

It’s crucial to distinguish between federal and private student loans. Historically, federal forgiveness programs almost exclusively apply to federal student loans. Private loans, issued by banks and other financial institutions, typically do not qualify for federal forgiveness programs. If you have private loans, you’ll need to explore refinancing options or other private lender relief programs.

Loan Type and Status

Many federal forgiveness programs specifically target Direct Loans. If you have older federal loans, such as FFEL Program loans or Perkins Loans, you might need to consolidate them into a Direct Consolidation Loan to become eligible for certain programs like PSLF or IDR plan forgiveness. Ensuring your loans are in good standing (not in default) is also typically a prerequisite.

Employment and Income Requirements

For programs like PSLF and IDR, your employment type (public service) and income level are critical. Keeping accurate records of your employment history, employer certifications, and income documentation will be essential. For IDR plans, annually recertifying your income and family size is mandatory to maintain eligibility and ensure your payments are correctly calculated.

Payment History

A consistent payment history is vital for many forgiveness programs. For PSLF, 120 qualifying payments are required. For IDR forgiveness, it’s 20 or 25 years of payments. While payment pauses (like the COVID-19 payment pause) have counted towards forgiveness for some programs, future payment requirements will likely revert to standard rules. It’s important to understand what constitutes a ‘qualifying payment’ for your specific program.

Residency and Citizenship

Generally, federal student aid and forgiveness programs are available to U.S. citizens and eligible non-citizens. Ensuring your residency and citizenship status is correctly documented will be important for any application process.

How to Apply for Student Loan Forgiveness: A Step-by-Step Guide

Applying for student loan forgiveness can seem daunting, but breaking it down into manageable steps can make the process clearer. This guide provides a general framework; always refer to the official Federal Student Aid website for the most up-to-date program-specific instructions.

Step 1: Determine Your Loan Type

Log in to StudentAid.gov using your FSA ID. Here, you can view all your federal student loans, their types, and current servicers. This is the first and most critical step, as it will determine which forgiveness programs you might be eligible for.

Step 2: Research Eligible Programs

Based on your loan types, employment history, and financial situation, research the various federal forgiveness programs (PSLF, IDR, Teacher Loan Forgiveness, TPD, etc.) to identify which ones you might qualify for. Pay close attention to the specific eligibility criteria for each program.

Step 3: Consolidate Loans if Necessary

If you have FFEL Program loans or Perkins Loans, and you wish to pursue PSLF or certain IDR plans, you may need to consolidate them into a Direct Consolidation Loan. This process can take several weeks, so plan accordingly. Be aware that consolidation can sometimes reset your payment count for forgiveness programs, though recent adjustments have aimed to mitigate this for some borrowers.

Step 4: Enroll in a Qualifying Repayment Plan

For PSLF and IDR forgiveness, you must be enrolled in a qualifying repayment plan. For PSLF, this typically means an IDR plan. For IDR forgiveness, you simply need to be on an IDR plan for the required duration. You can apply for or change your repayment plan through your loan servicer or on StudentAid.gov.

Step 5: Track Your Progress and Payments

This step is crucial, especially for PSLF. For PSLF, you must submit an Employment Certification Form (ECF) annually or whenever you change employers. This helps the Department of Education track your qualifying employment and payments. For IDR plans, ensure you recertify your income and family size annually to avoid capitalization of interest and maintain eligibility.

Step 6: Apply for Forgiveness

Once you believe you have met all the requirements for a specific program, you will need to submit a formal application for forgiveness. For PSLF, this is the PSLF & Temporary Expanded PSLF (TEPSLF) Certification & Application. For IDR forgiveness, your servicer should automatically process it once you reach the required number of payments, but it’s wise to monitor your account and inquire if you believe you’ve met the criteria.

Navigating Potential Debt Relief of Over $10,000

The prospect of receiving over $10,000 in debt relief is a significant motivator for many borrowers. While broad-based forgiveness of this magnitude is not currently enacted, the ongoing discussions and past actions of the government indicate it remains a possibility for student loan forgiveness 2026. Here’s how to position yourself:

Stay Informed

The student loan landscape is dynamic. Continuously monitor official sources like the Department of Education’s StudentAid.gov website, reputable financial news outlets, and congressional updates. Subscribing to email alerts from StudentAid.gov is highly recommended.

Understand Your Financial Situation

Know your total loan balance, interest rates, loan types, and current repayment plan. This information is foundational to understanding your options. Use the loan simulator tool on StudentAid.gov to explore different repayment scenarios.

Maintain Good Records

Keep meticulous records of all student loan documents, including promissory notes, payment histories, correspondence with servicers, and any employment certification forms. Digital copies are excellent, but also consider physical backups.

Seek Professional Advice

If your situation is complex, consider consulting with a non-profit credit counselor or a financial advisor specializing in student loan debt. Be wary of companies that charge upfront fees for forgiveness services; legitimate help is often free or low-cost.

Avoid Scams

Unfortunately, student loan forgiveness is a target for scammers. Never pay a fee for federal loan consolidation or forgiveness. The Department of Education and its servicers will never ask for your FSA ID password. Be skeptical of unsolicited calls or emails promising instant forgiveness.

The Future of Student Loan Debt and Higher Education Funding

Beyond immediate forgiveness, the discussion around student loans extends to broader reforms in higher education funding. Policymakers are exploring ways to make college more affordable and reduce the need for extensive borrowing in the first place. This includes proposals for tuition-free college, increased Pell Grant funding, and reforms to the federal student aid system.

While these long-term solutions may not directly impact your current loans, they shape the environment in which future student loan forgiveness 2026 policies will be considered. A more sustainable and equitable higher education financing system could reduce the prevalence of student loan debt in the future, lessening the need for large-scale forgiveness programs down the line.

Impact on Borrowers

For current borrowers, any form of significant debt relief, whether through existing programs or new initiatives, can have a profound impact. It can free up disposable income, improve credit scores, enable homeownership, and generally improve financial well-being. This economic ripple effect is often a key argument for proponents of forgiveness.

Challenges and Criticisms

It’s also important to acknowledge the challenges and criticisms surrounding student loan forgiveness. Concerns include the cost to taxpayers, fairness to those who have already paid off their loans, and the potential for moral hazard. These debates highlight the complexity of the issue and the various perspectives that policymakers must consider.

Conclusion: Preparing for Student Loan Forgiveness 2026

As we approach 2026, the potential for significant student loan forgiveness remains a topic of considerable interest and speculation. While no universal forgiveness program is currently enacted, the existing federal programs offer substantial relief for many eligible borrowers. By understanding these programs, staying informed about policy developments, and meticulously managing your loan information, you can strategically position yourself to benefit from any current or future debt relief opportunities.

Remember, proactive engagement is key. Regularly check your loan status, explore all available repayment and forgiveness options, and be prepared to act quickly if new programs or expansions are announced. The journey to financial freedom from student loan debt is a marathon, not a sprint, but with the right information and preparation, you can navigate it successfully. Keep an eye on official announcements and be ready to seize the opportunities that student loan forgiveness 2026 may bring.