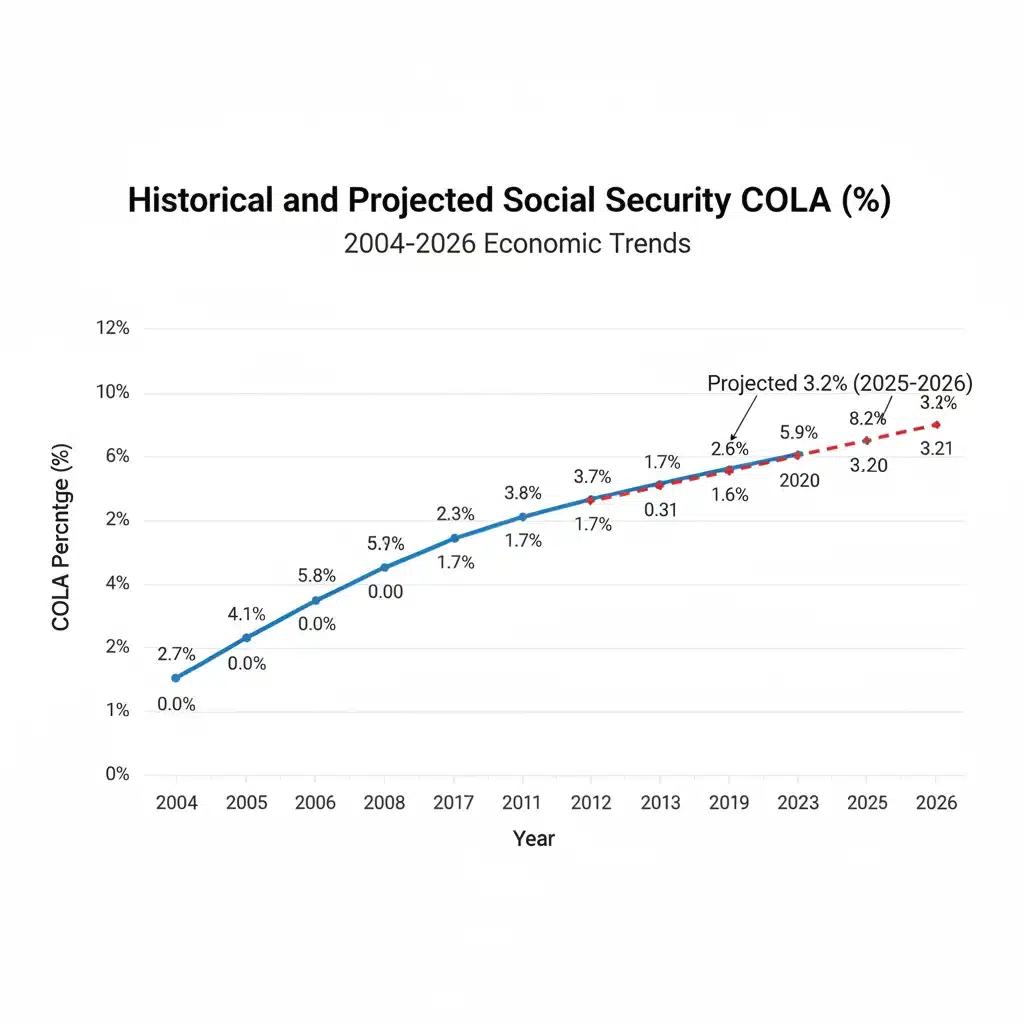

2026 Social Security COLA: What Retirees Must Know About Potential 3.2% Adjustments

Navigating the complexities of retirement finances requires constant vigilance and an understanding of the factors that impact your income. For millions of Americans, Social Security benefits form the bedrock of their financial security in their golden years. A critical component of these benefits is the Cost-of-Living Adjustment (COLA), an annual increase designed to help maintain the purchasing power of benefits against inflation. As we look ahead, the potential 2026 Social Security COLA is a topic of significant interest, with projections hinting at a 3.2% increase. This article will delve deep into what this potential adjustment means for retirees, the mechanisms behind COLA calculations, and how you can prepare for these changes.

Understanding the 2026 Social Security COLA is not just about a percentage; it’s about real money that affects your daily living expenses, your ability to afford healthcare, and your overall financial stability. A 3.2% increase, while seemingly modest, can have a substantial cumulative effect over time, providing much-needed relief in an economic landscape often characterized by rising costs. This comprehensive guide aims to equip you with the knowledge necessary to anticipate and adapt to these forthcoming changes, ensuring your retirement remains as comfortable and secure as possible.

The Significance of COLA for Retirees

The Cost-of-Living Adjustment (COLA) is more than just an annual raise; it’s a vital safeguard for retirees and other Social Security beneficiaries against the erosion of their purchasing power due to inflation. Without COLA, the fixed income of retirees would steadily decline in real value, making it increasingly difficult to afford essential goods and services. The Social Security Administration (SSA) calculates COLA annually, and its impact reverberates across various aspects of retirement life, from budgeting for groceries to planning for healthcare expenses.

For many, Social Security represents a primary, if not the sole, source of income in retirement. Therefore, any adjustment, particularly the projected 2026 Social Security COLA of 3.2%, is closely watched. This adjustment is crucial because it directly influences the monthly benefit amount received by millions. A higher COLA means more disposable income, potentially easing financial pressures and allowing for a more comfortable lifestyle. Conversely, a lower or non-existent COLA can strain budgets, forcing retirees to make difficult choices about their spending.

Beyond the immediate financial impact, COLA adjustments also play a psychological role. They offer a sense of security and stability, reassuring retirees that their benefits are designed to keep pace with the economy. This confidence is invaluable for long-term financial planning and overall well-being. Understanding how COLA is determined and what factors influence its size is therefore paramount for anyone relying on Social Security.

How COLA is Calculated: The CPI-W Index

The calculation of the Social Security COLA is a precise process overseen by the Social Security Administration, and it hinges on a specific economic indicator: the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). Unlike the broader Consumer Price Index (CPI-U) which measures inflation for all urban consumers, the CPI-W focuses on the spending patterns of a demographic that more closely aligns with Social Security beneficiaries.

Here’s a breakdown of how it works:

- The Baseline: The SSA compares the average CPI-W for the third quarter (July, August, and September) of the current year with the average CPI-W for the third quarter of the last year in which a COLA was granted.

- The Comparison: If the current year’s third-quarter CPI-W average is higher than the previous baseline, the percentage increase determines the COLA.

- No Decrease: Importantly, Social Security benefits can never decrease due to a COLA calculation. If the CPI-W shows a decline, the COLA will be zero, but benefits will not be reduced.

- Rounding: The final COLA percentage is rounded to the nearest one-tenth of one percent.

For the projected 2026 Social Security COLA of 3.2%, economic forecasters are making predictions based on anticipated inflation rates as measured by the CPI-W in the coming months and years. These forecasts are subject to change, as economic conditions can be volatile. However, early projections provide a valuable benchmark for retirees to begin their financial planning.

It’s vital to recognize that the CPI-W, while specifically chosen for COLA calculations, may not perfectly reflect the actual spending patterns and inflation experiences of all retirees. For instance, healthcare costs, which often consume a larger portion of a senior’s budget, may rise at a different rate than the overall CPI-W. This discrepancy is a frequent point of discussion and debate among policymakers and advocacy groups.

Factors Influencing the 2026 Social Security COLA

Several economic factors converge to determine the annual COLA. Understanding these influences can provide insight into why the 2026 Social Security COLA is projected at 3.2% and how future adjustments might unfold. The primary driver, as established, is inflation as measured by the CPI-W, but what influences the CPI-W itself?

Global Economic Conditions

The global economy plays a significant role. Supply chain disruptions, international trade policies, and geopolitical events can all impact the cost of goods and services domestically. For example, disruptions in oil production can lead to higher energy prices, which then feed into the cost of transportation and manufacturing, ultimately affecting consumer prices.

Domestic Economic Trends

Within the United States, factors such as consumer demand, wage growth, and unemployment rates are crucial. Strong consumer demand, coupled with robust wage growth, can push prices higher. Conversely, a slowdown in the economy might lead to lower inflation. The Federal Reserve’s monetary policy, including interest rate decisions, also heavily influences economic activity and, consequently, inflation.

Energy Prices

The cost of energy, particularly gasoline and utilities, has a disproportionate impact on the CPI-W because these are essential expenditures for most households. Significant fluctuations in oil prices, for instance, can quickly shift inflation trends and thus impact the 2026 Social Security COLA.

Food Prices

Similarly, food prices are a major component of the CPI-W. Factors such as weather patterns affecting agricultural yields, transportation costs, and global demand can all contribute to changes in the cost of food, directly influencing the COLA calculation.

Housing Costs

Rent and housing-related expenses are another substantial category within the CPI-W. Increases in housing costs, driven by factors like population growth, interest rates, and construction costs, can significantly contribute to overall inflation.

Forecasting the 2026 Social Security COLA requires analysts to weigh these complex and interconnected factors. While a 3.2% projection offers a preliminary figure, it’s essential for retirees to stay informed about ongoing economic developments, as these can alter the final adjustment.

Understanding the Impact of a 3.2% COLA on Your Benefits

A 3.2% increase in Social Security benefits, as projected for the 2026 Social Security COLA, might seem like a small number at first glance, but its cumulative effect can be significant for retirees. To truly grasp its impact, it’s helpful to consider both the immediate monthly increase and its long-term implications.

Immediate Monthly Impact

Let’s illustrate with an example. If a retiree currently receives $1,800 per month in Social Security benefits, a 3.2% COLA would translate to an additional $57.60 per month ($1,800 x 0.032). This would bring their new monthly benefit to $1,857.60. While this might not seem like a vast sum, for individuals on a fixed income, every dollar counts. This extra amount can help cover rising costs of daily necessities, medications, or even allow for a small discretionary expense.

For those with higher current benefits, the absolute dollar increase will be greater. For instance, a retiree receiving $2,500 per month would see an increase of $80.00, bringing their new benefit to $2,580.00. Conversely, those with lower benefits will see a smaller dollar increase, highlighting the importance of every percentage point in the COLA.

Long-Term Financial Implications

Over a year, that $57.60 monthly increase adds up to $691.20 annually. Over several years, especially when compounded with future COLA adjustments, the effect becomes even more pronounced. This cumulative increase helps maintain purchasing power over the span of a retirement that could last for two or three decades.

The 2026 Social Security COLA, and subsequent adjustments, are designed to prevent benefits from being eroded by inflation. Without these increases, the real value of Social Security benefits would diminish significantly over time. This means that while a 3.2% COLA might not make retirees wealthy, it helps them maintain their standard of living and cope with the rising cost of goods and services, particularly in areas like healthcare and housing, which tend to increase steadily.

It’s also important to consider how COLA impacts other aspects of retirement planning, such as budgeting and withdrawal strategies from other retirement accounts. A predictable increase in Social Security can influence how much retirees need to draw from their savings, potentially prolonging the lifespan of their investment portfolios.

Potential Challenges and Considerations for Retirees

While a positive 2026 Social Security COLA is generally welcome news, retirees must also be aware of potential challenges and considerations that can affect their overall financial picture. The COLA is just one piece of the retirement income puzzle, and other factors can influence its net benefit.

Medicare Part B Premiums

One of the most significant considerations is the potential increase in Medicare Part B premiums. By law, if a retiree’s Part B premium increases, and they are protected by the ‘hold harmless’ provision (meaning their Part B premium increase cannot reduce their net Social Security benefit below the previous year’s level), the COLA increase might be partially or entirely absorbed by the premium hike. This is especially relevant for those whose Part B premiums are deducted directly from their Social Security checks.

For individuals not protected by the hold harmless provision (e.g., new Medicare enrollees, those paying higher income-related monthly adjustment amounts, or those who don’t have their premiums deducted from Social Security), the Part B premium increase will be an additional out-of-pocket expense, regardless of the COLA.

Income Tax on Social Security Benefits

Another crucial factor is the taxation of Social Security benefits. Depending on a retiree’s ‘provisional income’ (which includes adjusted gross income, tax-exempt interest, and half of their Social Security benefits), a portion of their Social Security benefits may be subject to federal income tax. An increase due to the 2026 Social Security COLA could potentially push some retirees into a higher provisional income bracket, making more of their benefits taxable, or increasing the percentage of benefits that are taxable (up to 85%).

It’s essential for retirees to understand their tax situation and consult with a tax professional to determine how an increased benefit might affect their tax liability. State income taxes on Social Security benefits also vary, with some states taxing benefits and others not.

Impact on Other Means-Tested Benefits

For retirees receiving other means-tested government benefits (e.g., Medicaid, Supplemental Security Income (SSI), or certain housing assistance programs), an increase in Social Security income due to the 2026 Social Security COLA could potentially affect their eligibility or the amount of those other benefits. These programs often have strict income thresholds, and even a modest increase in Social Security can sometimes push recipients over these limits, leading to a reduction or loss of other crucial support.

This is a complex area, and individuals receiving multiple forms of government assistance should carefully review how a COLA increase might interact with their other benefits. Proactive planning and seeking advice from relevant agencies are recommended.

Strategies for Financial Planning with the 2026 Social Security COLA

Given the potential 3.2% 2026 Social Security COLA, retirees have an opportunity to fine-tune their financial strategies. Proactive planning can help maximize the benefit of this adjustment and mitigate any potential challenges.

Review Your Budget

The first step is to revisit your household budget. Incorporate the projected COLA increase into your income calculations. How will this extra income impact your monthly cash flow? Identify areas where you might allocate the additional funds, whether it’s covering rising costs, building an emergency fund, or even allocating towards small discretionary expenses that enhance your quality of life.

Pay particular attention to categories where inflation has been most pronounced, such as groceries, utilities, and healthcare. The COLA is designed to offset these increases, so ensure your budget reflects realistic current costs.

Assess Your Medicare Part B Premiums

As discussed, Medicare Part B premiums are a critical component. Stay informed about the projected Part B premium increases for 2026. If you are subject to the ‘hold harmless’ provision, understand how the COLA might be partially absorbed. If you are not protected by this provision, budget for the full premium increase as an additional expense.

Consider exploring Medicare Advantage plans or Medigap policies to ensure you have comprehensive coverage that aligns with your budget and healthcare needs. These choices can significantly impact your out-of-pocket medical expenses.

Consult a Tax Professional

Given the potential for increased tax liability on Social Security benefits, it is highly advisable to consult with a tax professional. They can help you understand how the 2026 Social Security COLA might affect your provisional income and overall tax burden. They can also advise on strategies to minimize taxes, such as qualified charitable distributions from IRAs, if applicable.

Understanding your tax situation before the year begins allows for proactive adjustments, rather than surprises during tax season.

Re-evaluate Your Investment Portfolio

If you have other retirement savings, consider how the COLA impacts your overall withdrawal strategy. A slightly higher Social Security benefit might allow you to draw less from your investment portfolio, potentially extending its longevity. Conversely, if inflation continues to outpace COLA, you might need to adjust your withdrawal rates from other accounts to maintain your desired lifestyle.

Work with a financial advisor to ensure your investment portfolio remains aligned with your risk tolerance and long-term financial goals, especially in an evolving economic environment.

Stay Informed About Economic Trends

Economic forecasts are dynamic. Stay updated on official announcements from the Social Security Administration regarding the final COLA for 2026. Additionally, keep an eye on broader economic indicators, such as inflation reports and interest rate decisions, as these can provide context for future adjustments.

Reliable sources for this information include the Social Security Administration’s official website, the Bureau of Labor Statistics, and reputable financial news outlets.

Advocacy and Future of Social Security

The discussion around the 2026 Social Security COLA and future adjustments is part of a larger, ongoing conversation about the long-term solvency and adequacy of Social Security. While COLA helps benefits keep pace with inflation, there are broader challenges and proposals that retirees should be aware of.

The CPI-W Debate

As mentioned earlier, some critics argue that the CPI-W does not accurately reflect the inflation experienced by seniors, particularly due to their heavier spending on healthcare. Proposals to switch to an alternative index, such as the Consumer Price Index for the Elderly (CPI-E), have been put forth. The CPI-E specifically tracks the spending habits of those aged 62 and older. While this could potentially result in higher COLA increases for retirees, it also has implications for the overall solvency of the Social Security trust funds.

Long-Term Solvency Concerns

Social Security faces long-term financial challenges due to demographic shifts, including lower birth rates and increased longevity. Without legislative action, the trust funds are projected to be unable to pay 100% of promised benefits at some point in the future. Various proposals to address this include:

- Raising the Full Retirement Age: Gradually increasing the age at which individuals can claim full Social Security benefits.

- Adjusting the Wage Base: Increasing the amount of earnings subject to Social Security taxes.

- Modifying Benefit Formulas: Changing how benefits are calculated for future retirees.

- Means-Testing: Reducing benefits for higher-income beneficiaries.

- General Revenue Infusion: Using general tax revenues to supplement Social Security funding.

These discussions are complex and often politically charged. Retirees and future beneficiaries have a vested interest in staying informed about these debates and engaging with their elected officials to advocate for solutions that ensure the program’s strength for generations to come.

The Role of Advocacy Groups

Organizations like AARP and the National Council on Aging actively advocate for policies that protect and strengthen Social Security benefits, including fair COLA adjustments. These groups often conduct research, lobby lawmakers, and educate the public on issues related to retirement security. Supporting or following such organizations can provide valuable insights and avenues for collective action.

The 2026 Social Security COLA is a snapshot within this broader context. While the annual adjustment addresses immediate inflation concerns, the long-term health of Social Security requires ongoing attention and thoughtful policy decisions.

Conclusion: Preparing for Your Financial Future with the 2026 COLA

The projected 3.2% 2026 Social Security COLA represents a crucial adjustment for millions of retirees, designed to help their benefits keep pace with the rising cost of living. While not a dramatic increase, it provides a vital boost that can significantly impact monthly budgets and long-term financial stability. Understanding the mechanisms behind COLA, the factors influencing its calculation, and its potential effects on your personal finances is paramount for effective retirement planning.

As we’ve explored, the COLA is a complex interplay of economic indicators, primarily the CPI-W, influenced by global and domestic economic trends, energy costs, and food and housing prices. While a 3.2% increase offers a positive outlook, retirees must also remain mindful of potential offsets, such as rising Medicare Part B premiums and increased income tax liability on benefits. These considerations underscore the importance of a holistic approach to retirement financial management.

Proactive strategies, including a thorough review of your budget, careful assessment of Medicare costs, consultation with tax and financial professionals, and continuous monitoring of economic trends, are essential. By taking these steps, retirees can effectively integrate the 2026 Social Security COLA into their financial plans, ensuring they are well-prepared for any adjustments and can maintain their desired quality of life.

Ultimately, Social Security remains a cornerstone of retirement security for many. Staying informed, planning meticulously, and engaging in the ongoing dialogue about the program’s future will empower you to navigate the evolving financial landscape with confidence and peace of mind. The 2026 Social Security COLA is more than just a number; it’s a key element in the ongoing journey of securing a stable and comfortable retirement.