Optimize Your 2026 Retirement: Maximize Social Security & 401k

Optimizing Your 2026 Retirement Portfolio: Insider Tips for Maximizing Social Security Benefits and 401k Contributions

The year 2026 might seem like a distant future, but for those nearing retirement, it’s a critical benchmark. The decisions you make today regarding your Social Security benefits and 401k contributions will profoundly impact the quality of your retirement. This comprehensive guide delves into insider tips and strategic approaches to ensure your 2026 retirement optimization is on track, maximizing every available dollar and securing your financial independence.

Retirement planning is not a one-size-fits-all endeavor. It requires careful consideration of individual circumstances, risk tolerance, and long-term goals. As we approach 2026, economic landscapes, legislative changes, and personal health factors can all influence the best course of action. Our aim here is to equip you with the knowledge and actionable strategies to navigate these complexities effectively.

Understanding the Pillars of Your 2026 Retirement Portfolio

Before diving into specific optimization techniques, it’s crucial to understand the two main pillars of most American retirement plans: Social Security and 401k accounts. While seemingly straightforward, both have intricate rules and strategies that, when understood and applied correctly, can significantly boost your retirement income.

The Role of Social Security in Your Retirement

Social Security is designed to replace a portion of your pre-retirement income. However, the amount you receive depends heavily on your earnings history and, most critically, when you decide to start claiming benefits. Many retirees make the mistake of claiming benefits too early, leaving substantial income on the table.

The Power of Your 401k

Your 401k, often employer-sponsored, is a powerful savings vehicle. Its tax-advantaged growth, coupled with potential employer matching contributions, makes it an indispensable tool for building a robust retirement nest egg. Strategic contributions and investment choices within your 401k are paramount for effective 2026 retirement optimization.

Maximizing Social Security Benefits for Your 2026 Retirement

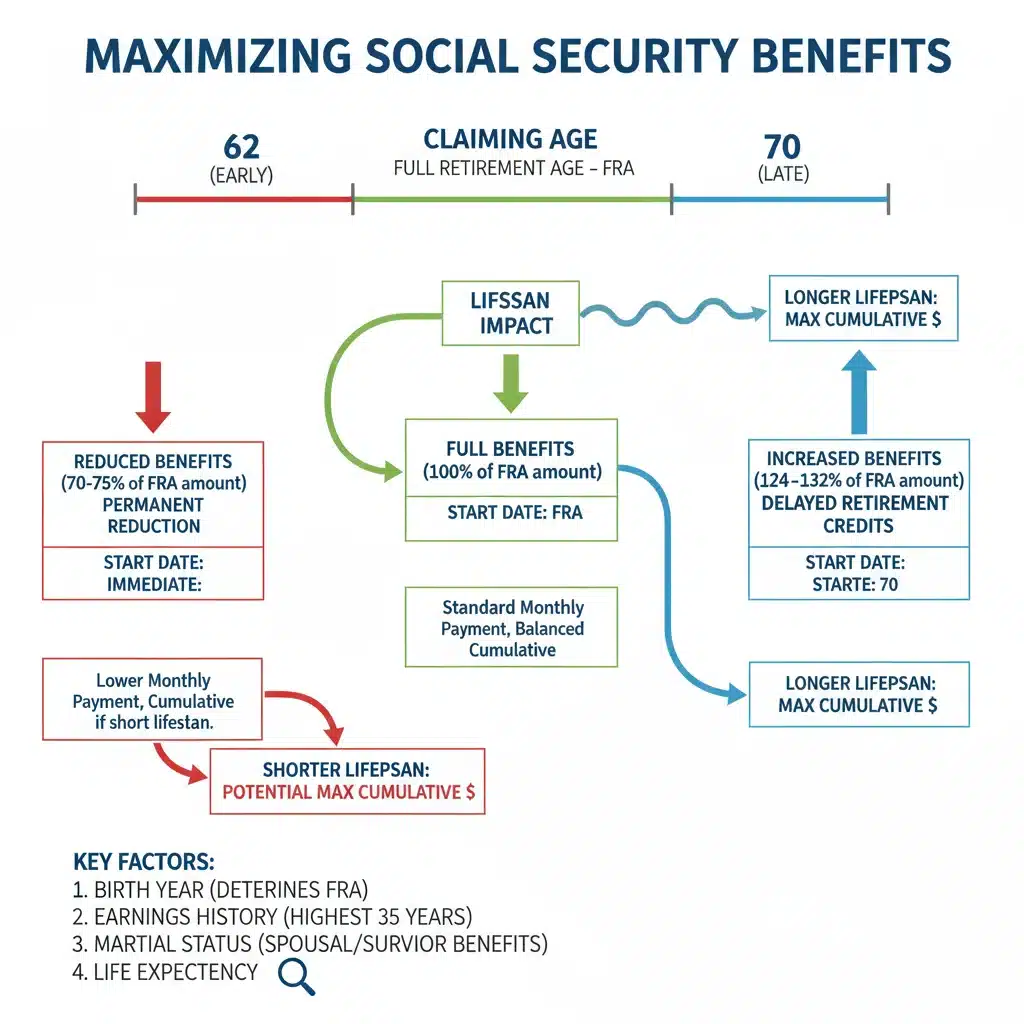

One of the most impactful decisions you’ll make regarding your retirement income is when to claim Social Security. The difference between claiming at age 62 (the earliest) and age 70 (the latest to receive delayed retirement credits) can be thousands of dollars per year, a sum that accumulates significantly over a typical retirement lifespan.

Understanding Full Retirement Age (FRA)

Your Full Retirement Age (FRA) is the age at which you are entitled to 100% of your Social Security benefits. For those born between 1943 and 1954, FRA is 66. For those born between 1955 and 1959, it gradually increases, reaching 67 for those born in 1960 or later. Knowing your FRA is the first step in strategic claiming.

The Benefits of Delaying Social Security

For every year you delay claiming benefits past your FRA, up to age 70, your benefit amount increases by approximately 8% per year. This is a guaranteed, inflation-adjusted return that is hard to beat in any investment market. For someone with an FRA of 67, delaying until 70 means a 24% increase in their monthly benefit for the rest of their life.

Consider this: if your FRA benefit is $2,000 per month, delaying for three years could mean an extra $480 per month, or nearly $5,800 per year. Over a 20-year retirement, this amounts to over $115,000 in additional income. This is a cornerstone of 2026 retirement optimization.

Spousal and Survivor Benefits

If you are married, divorced, or widowed, there are additional Social Security strategies to consider. Spousal benefits allow one spouse to claim benefits based on the other spouse’s work record, potentially even if they haven’t worked or have a lower earnings record. Survivor benefits provide crucial support to surviving spouses or ex-spouses.

- Claiming Spousal Benefits: If your spouse has a higher earnings record, you might be able to claim a spousal benefit equal to 50% of their FRA benefit when they file for their own benefits, provided you are at least your FRA.

- "File and Suspend" (for those eligible before 2016): While largely phased out, some individuals born before January 2, 1954, may still benefit from "file and suspend" strategies, allowing one spouse to file for benefits, triggering spousal benefits for the other, while their own benefits continue to grow. This is complex and requires expert advice.

- Survivor Benefits: Widows and widowers can claim 100% of their deceased spouse’s benefit. The optimal time to claim survivor benefits might differ from claiming your own. It’s often possible to claim one benefit (e.g., survivor) while letting your own continue to grow until age 70.

These strategies underscore the importance of understanding the nuances of Social Security to truly maximize your retirement income. For your 2026 retirement optimization, a detailed analysis of your personal and family situation is essential.

Strategic 401k Contributions for a Robust 2026 Retirement

While Social Security provides a foundation, your 401k is where significant wealth accumulation often occurs. Proactive and strategic contributions, especially in the years leading up to 2026, can dramatically impact your financial security.

Maximize Employer Matching Contributions

This is arguably the easiest and most effective way to boost your 401k. If your employer offers a matching contribution (e.g., they match 50 cents on the dollar up to 6% of your salary), failing to contribute enough to receive the full match is essentially leaving free money on the table. This should be the absolute minimum you contribute for optimal 2026 retirement optimization.

Increase Contributions Annually

Even small, consistent increases in your contribution rate can have a substantial impact over time due to the power of compounding. If you’re not already maxing out your 401k, aim to increase your contribution by 1% or 2% of your salary each year. As your income grows, try to allocate a portion of that raise directly to your 401k.

Leverage Catch-Up Contributions

For those aged 50 and over, the IRS allows "catch-up" contributions to 401k plans. In 2023, this additional contribution amount was $7,500, on top of the standard $22,500 limit, totaling $30,000. These catch-up contributions are an invaluable tool for boosting your savings in the final years before retirement, making a significant difference for your 2026 retirement optimization.

Understand Roth 401k vs. Traditional 401k

Many employers now offer both traditional and Roth 401k options. Understanding the tax implications of each is crucial for your long-term strategy:

- Traditional 401k: Contributions are made pre-tax, reducing your current taxable income. Taxes are paid when you withdraw funds in retirement. This can be advantageous if you expect to be in a lower tax bracket in retirement than you are now.

- Roth 401k: Contributions are made with after-tax dollars, meaning your withdrawals in retirement are tax-free, provided you meet certain conditions. This is often beneficial if you expect to be in a higher tax bracket in retirement.

The choice between these two depends on your current income, anticipated retirement income, and future tax rate expectations. Consulting a financial advisor can help you determine the best option for your 2026 retirement optimization.

Review and Rebalance Your Investments

As you near retirement, your investment strategy within your 401k should shift. While younger investors can afford to take on more risk for potentially higher returns, those approaching retirement typically need to de-risk their portfolio to protect accumulated capital. This usually involves shifting from a higher allocation of stocks to a higher allocation of bonds and cash equivalents.

Regularly review your 401k investments, at least annually, and rebalance as needed to align with your risk tolerance and timeline to 2026. This proactive management is key to safeguarding your savings.

Integrating Social Security and 401k Strategies for Optimal 2026 Retirement

The true power of 2026 retirement optimization lies in integrating your Social Security and 401k strategies. They are not isolated components but rather interconnected elements of your overall financial plan.

Bridging the Gap with 401k Funds

If you decide to delay Social Security benefits until age 70 to maximize your monthly payments, you’ll need a source of income to cover the years between your desired retirement age and when you start claiming Social Security. Your 401k can serve as this bridge.

By strategically withdrawing from your 401k during these "gap years," you can allow your Social Security benefits to grow significantly. This requires careful planning to avoid depleting your 401k too quickly or incurring unnecessary taxes.

Tax-Efficient Withdrawal Strategies

Understanding how withdrawals from your 401k will be taxed is crucial. Traditional 401k withdrawals are taxed as ordinary income. Roth 401k withdrawals are tax-free. By having a combination of tax-deferred (Traditional 401k) and tax-free (Roth 401k/IRA) accounts, you gain flexibility in managing your tax burden in retirement.

For example, in years where you have lower income, you might withdraw more from a traditional 401k to stay in a lower tax bracket. In years where you need more income or anticipate higher taxes, you might withdraw from a Roth account. This tax diversification is a sophisticated aspect of 2026 retirement optimization.

Considering Other Factors for Your 2026 Retirement

While Social Security and 401k are central, a holistic approach to 2026 retirement optimization involves several other critical considerations.

Healthcare Costs in Retirement

Healthcare is often one of the largest and most unpredictable expenses in retirement. Medicare will cover a significant portion, but it won’t cover everything. Long-term care insurance, health savings accounts (HSAs), and careful budgeting for out-of-pocket medical costs are essential components of your retirement plan.

An HSA, if you are eligible, is a triple-tax-advantaged account (tax-deductible contributions, tax-free growth, tax-free withdrawals for qualified medical expenses) that can be a powerful tool for covering healthcare costs in retirement, even serving as an additional investment vehicle.

Debt Management

Entering retirement debt-free (or with minimal debt) significantly reduces your financial stress and allows your retirement income to go further. Prioritize paying off high-interest debts like credit card balances and personal loans before 2026. Consider accelerating mortgage payments if feasible.

Part-Time Work or "Retirement Gigs"

Many individuals choose to work part-time in retirement, not just for financial reasons but also for social engagement and mental stimulation. This can provide valuable supplemental income, allowing you to delay claiming Social Security or take smaller withdrawals from your 401k, thereby extending the longevity of your savings.

Be aware of Social Security’s earnings limit if you claim benefits before your FRA and continue to work. Exceeding this limit can temporarily reduce your benefits, though they are recalculated at your FRA.

Estate Planning

As you finalize your retirement plans, ensure your estate plan is up-to-date. This includes wills, trusts, powers of attorney, and beneficiary designations for your retirement accounts. Proper estate planning ensures your assets are distributed according to your wishes and can minimize taxes for your heirs.

The Importance of Professional Guidance for 2026 Retirement Optimization

Navigating the complexities of Social Security, 401k rules, tax laws, and investment strategies can be overwhelming. A qualified financial advisor specializing in retirement planning can provide invaluable assistance. They can help you:

- Develop a personalized retirement income strategy.

- Analyze your Social Security claiming options to maximize benefits.

- Optimize your 401k contributions and investment allocations.

- Create a tax-efficient withdrawal strategy for retirement.

- Factor in healthcare costs and other potential expenses.

- Review and update your estate plan.

The investment in professional advice often pays for itself many times over through increased benefits and optimized financial outcomes. For a robust 2026 retirement optimization, consider this a crucial step.

Actionable Steps to Take Today for Your 2026 Retirement

Don’t wait until 2026 to start planning. Here are immediate steps you can take:

- Review Your Social Security Statement: Access your statement at ssa.gov/myaccount to check your earnings history and estimated benefits. Correct any errors promptly.

- Assess Your 401k Contributions: Are you contributing enough to get the full employer match? Can you increase your contribution by 1-2%? Are you taking advantage of catch-up contributions if eligible?

- Understand Your Investment Mix: Review your 401k’s asset allocation. Is it appropriate for your age and risk tolerance given your 2026 retirement timeline?

- Project Your Retirement Expenses: Create a realistic budget for your retirement. This will help you determine how much income you’ll need.

- Consider Professional Advice: Schedule a consultation with a fee-only financial advisor to discuss your specific situation and develop a tailored retirement plan.

- Educate Yourself: Continuously learn about retirement planning strategies, tax law changes, and investment options.

Conclusion: A Secure 2026 Retirement Awaits

Achieving optimal 2026 retirement optimization requires foresight, discipline, and a willingness to make informed decisions. By strategically maximizing your Social Security benefits and diligently contributing to and managing your 401k, you lay the groundwork for a comfortable and secure retirement.

Remember, every dollar saved and every strategic decision made today contributes to a more financially independent tomorrow. Start planning, stay informed, and don’t hesitate to seek expert guidance. Your future self will thank you.

in 2026: Advanced Strategies for 10% Annual Growth")