2026 US Housing Market Forecast: Mortgage Rates & Investment Insights

The housing market is a dynamic and multifaceted entity, constantly influenced by a myriad of economic, social, and political factors. As we cast our gaze towards 2026, prospective homebuyers, current homeowners, and savvy investors are all keenly interested in understanding what lies ahead. This comprehensive analysis will delve into the anticipated landscape of the 2026 Housing Market in the United States, offering a data-driven perspective on mortgage rate predictions, identifying key investment opportunities, and dissecting regional trends that will shape the real estate future.

Understanding the trajectory of the 2026 Housing Market requires a deep dive into several interconnected components. We’ll explore the prevailing economic conditions, the Federal Reserve’s monetary policy, demographic shifts, and supply-demand dynamics. Our goal is to provide a clear, actionable roadmap for navigating what promises to be an intriguing period for real estate.

Understanding the Macroeconomic Landscape Influencing the 2026 Housing Market

The health of the broader economy is inextricably linked to the performance of the housing market. Several macroeconomic indicators will play a pivotal role in shaping the 2026 Housing Market. These include inflation rates, GDP growth, employment figures, and consumer confidence. A robust economy generally supports a strong housing market, driven by job growth and increased purchasing power. Conversely, economic downturns can lead to reduced demand and softer prices.

Inflation and its Impact on Housing

Inflation has been a significant concern in recent years, prompting central banks to take decisive action. By 2026, many economists anticipate that inflation will have moderated closer to the Federal Reserve’s target of 2%. A stable, lower inflation environment is crucial for normalizing interest rates and, consequently, mortgage rates. Persistent high inflation, however, could lead to continued monetary tightening, which would put upward pressure on borrowing costs and temper housing demand. The delicate balance between economic growth and inflation control will be a primary driver for the 2026 Housing Market.

GDP Growth and Employment Trends

Gross Domestic Product (GDP) growth indicates the overall economic output of the nation. Steady, positive GDP growth typically translates to a healthy job market, which is a fundamental pillar of housing demand. When people are employed and earning stable incomes, they are more likely to purchase homes. Looking at the 2026 Housing Market, we expect continued, albeit perhaps slower, GDP growth compared to post-pandemic surges. This sustained growth, coupled with resilient employment figures, should provide a foundational level of demand. However, regional disparities in job growth will inevitably lead to varied housing market performance across the country.

Consumer Confidence and Housing Sentiment

Beyond the hard economic data, consumer confidence plays a psychological yet powerful role. When consumers feel secure about their financial future and the broader economy, they are more inclined to make significant investments like buying a home. Conversely, uncertainty can lead to hesitation and a slowdown in market activity. Surveys on consumer sentiment will be vital indicators for predicting the emotional pulse of the 2026 Housing Market, influencing everything from buying urgency to selling expectations.

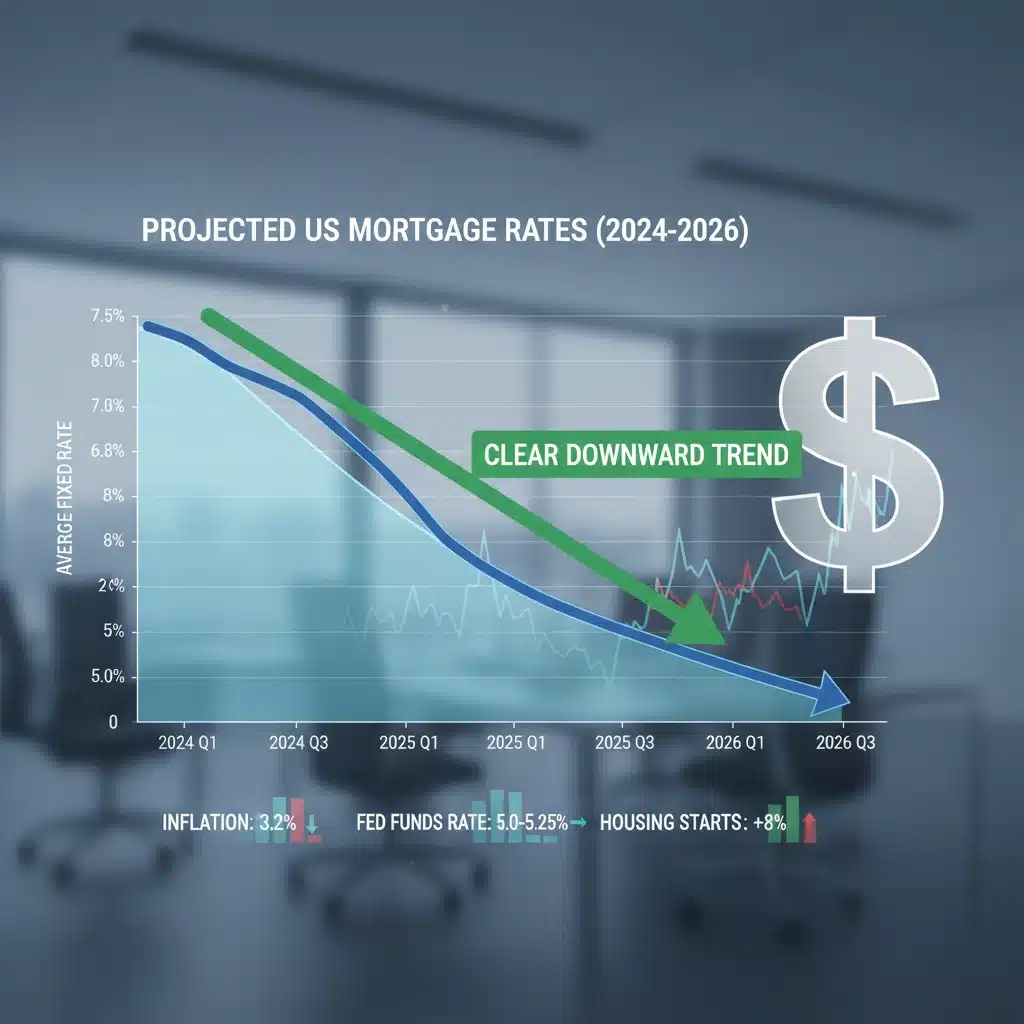

Mortgage Rate Predictions for the 2026 Housing Market

Perhaps the most critical factor for many prospective buyers is the trajectory of mortgage rates. These rates directly impact affordability and borrowing power. Analyzing the Federal Reserve’s anticipated actions and broader economic trends provides insight into what to expect for the 2026 Housing Market.

The Federal Reserve’s Role and Monetary Policy

The Federal Reserve’s policy decisions, particularly regarding the federal funds rate, have a profound influence on mortgage rates. While mortgage rates don’t directly mirror the federal funds rate, they tend to move in the same direction. By 2026, it is widely expected that the Fed will have concluded its tightening cycle and may even be in a phase of modest rate cuts, assuming inflation remains under control. This anticipated shift would likely lead to a more favorable environment for mortgage borrowers.

Our projections suggest that 30-year fixed-rate mortgages, which have hovered at elevated levels in recent times, could see a gradual decline. While a return to the historically low rates of the pandemic era is unlikely, we could see rates settling into a more moderate range, potentially between 5.5% and 6.5% for well-qualified borrowers. This moderation would significantly improve affordability, potentially unlocking demand that has been sidelined by higher rates.

Factors Influencing Mortgage Rate Volatility

Despite the general outlook for moderation, several factors could introduce volatility into mortgage rates in the 2026 Housing Market. These include:

- Unexpected Inflation Surges: A resurgence of inflation would likely prompt the Fed to reconsider its rate-cutting plans, pushing mortgage rates higher.

- Global Economic Shocks: Geopolitical events or significant economic downturns in other major economies could impact bond markets, which in turn affect mortgage rates.

- Treasury Yields: Mortgage rates are closely tied to the yield on 10-year Treasury bonds. Any significant shifts in these yields, driven by investor sentiment or economic data, will directly influence mortgage costs.

Buyers in the 2026 Housing Market should remain vigilant and consider locking in rates when favorable conditions arise, while also being prepared for potential rate fluctuations.

Investment Opportunities in the 2026 Housing Market

For investors, the 2026 Housing Market presents a landscape of both challenges and opportunities. Identifying the right strategies and locations will be key to success.

Identifying Growth Markets and Emerging Trends

Not all housing markets are created equal. By 2026, certain regions are expected to outperform others due to strong economic fundamentals, population growth, and relative affordability. Consider areas experiencing:

- Job Market Expansion: Cities attracting major companies or experiencing significant growth in high-paying sectors (e.g., tech, healthcare, advanced manufacturing) will likely see increased housing demand.

- In-migration Trends: Regions with a net positive influx of residents, often driven by affordability or lifestyle factors, tend to have stronger housing markets.

- Infrastructure Development: Investments in new transportation, utilities, or public amenities can significantly boost property values in surrounding areas.

Investors should look beyond the traditional coastal hubs and consider secondary and tertiary markets that offer greater potential for appreciation and rental yield in the 2026 Housing Market.

Types of Investment Strategies to Consider

Depending on risk tolerance and financial goals, various investment strategies could prove fruitful in the 2026 Housing Market:

- Rental Properties: With continued population growth and potentially moderating purchase prices, single-family and multi-family rental properties could offer attractive cash flow and long-term appreciation. Focus on areas with strong renter demand and favorable landlord-tenant laws.

- Fix-and-Flip: For experienced investors, the fix-and-flip strategy might see renewed interest if acquisition costs stabilize and buyer demand remains robust. However, construction costs and labor availability will need careful management.

- BRRRR Method (Buy, Rehab, Rent, Refinance, Repeat): This strategy allows investors to scale their portfolios by leveraging equity. The anticipated moderation in mortgage rates could make the refinance component more appealing.

- Short-Term Rentals (STRs): While regulations vary widely, certain tourist destinations or business travel hubs may offer lucrative opportunities for STRs, especially if travel continues its post-pandemic recovery.

Due diligence is paramount. Investors should thoroughly research local market conditions, rental demand, property taxes, and potential returns before committing to any strategy in the 2026 Housing Market.

Regional Variations: A Closer Look at the US Housing Market in 2026

The United States is a vast country, and the housing market is far from monolithic. What happens in one region may not reflect the situation in another. Understanding these regional nuances is critical for accurate predictions regarding the 2026 Housing Market.

The Sun Belt Continues to Shine

The Sun Belt states, particularly in the Southeast and Southwest, are expected to continue their strong performance. States like Florida, Texas, Arizona, and parts of the Carolinas have seen significant population growth, driven by job creation, lower cost of living, and favorable climates. This influx of residents fuels demand for housing, supporting both sales prices and rental rates. However, rapid growth can also lead to affordability challenges and increased competition, so investors and buyers should monitor supply levels carefully within the 2026 Housing Market in these areas.

Northeast and West Coast: Resilience and Nuance

Markets in the Northeast and on the West Coast, while historically expensive, are known for their strong economies and high-paying job sectors. Major metropolitan areas like New York, Boston, San Francisco, and Seattle will likely remain desirable, but affordability will continue to be a significant barrier for many. We anticipate a more stable, albeit slower, appreciation in these regions for the 2026 Housing Market. Some suburban and exurban areas outside these major cities may see continued interest as remote work trends persist, offering a balance of accessibility and relative value.

Midwest: Affordability and Steady Growth

The Midwest often offers a compelling combination of affordability and steady economic growth. Many cities in this region have diversified economies and a lower cost of living compared to coastal areas. This makes them attractive to first-time homebuyers and investors seeking higher rental yields. While not typically experiencing the dramatic price surges of the Sun Belt, the Midwest could provide stable, consistent returns in the 2026 Housing Market, especially in cities with strong education sectors or growing manufacturing bases.

Supply and Demand Dynamics in the 2026 Housing Market

The fundamental economic principles of supply and demand are always at play in the housing market. Understanding how these forces will evolve by 2026 is crucial for predicting market conditions.

Housing Supply: Inventory Challenges Persist

Despite increased construction activity, the US has faced a persistent housing supply shortage for years. This deficit is due to a combination of factors, including underbuilding since the 2008 financial crisis, restrictive zoning laws, and labor shortages in the construction industry. While new construction is expected to continue its upward trend, it may not fully alleviate the existing supply gap by 2026. This ongoing limited inventory, particularly in desirable locations, will likely continue to put upward pressure on prices, even if demand moderates due to higher rates.

The type of housing being built also matters. There’s a growing need for entry-level and mid-range homes, but builders often find it more profitable to construct larger, more expensive properties. This mismatch can exacerbate affordability issues in the 2026 Housing Market for first-time buyers.

Housing Demand: Demographic Shifts and Affordability

Demand in the 2026 Housing Market will be driven by several demographic factors:

- Millennials and Gen Z: These generations represent a massive cohort entering prime homebuying years. While many have been priced out of the market or delayed homeownership, moderating mortgage rates and potential price stabilization could bring more of them into the market.

- Household Formation: The rate at which new households are formed directly impacts housing demand. A strong economy and growing population contribute to increased household formation.

- Remote Work: The ongoing flexibility of remote or hybrid work continues to influence where people choose to live, potentially spreading demand to more affordable, less dense areas. This trend could reshape demand patterns in the 2026 Housing Market, favoring suburbs and smaller cities.

Affordability remains the biggest constraint on demand. Even with potentially lower mortgage rates, high home prices and rising property taxes can make homeownership challenging. Innovative solutions, such as shared equity programs, accessory dwelling units (ADUs), and denser housing developments, will be crucial for addressing this in the 2026 Housing Market.

Potential Risks and Headwinds for the 2026 Housing Market

While our outlook for the 2026 Housing Market is generally optimistic, it’s essential to acknowledge potential risks that could alter the trajectory. Prudent buyers and investors will consider these factors when making decisions.

Economic Recession Risks

Although a soft landing is widely anticipated, the risk of an economic recession cannot be entirely dismissed. An unexpected downturn could lead to job losses, decreased consumer confidence, and a significant reduction in housing demand, potentially causing price corrections. The global economic environment and unforeseen geopolitical events could also trigger such a scenario, impacting the 2026 Housing Market.

Interest Rate Surprises

While our forecast anticipates moderating mortgage rates, persistent inflation or other economic pressures could force the Federal Reserve to maintain higher interest rates for longer than expected, or even resume rate hikes. Such a scenario would dampen affordability and put downward pressure on housing activity in the 2026 Housing Market.

Geopolitical Instability

Global conflicts and geopolitical tensions can have far-reaching effects on economies, including energy prices, supply chains, and investor sentiment. Significant instability could introduce uncertainty into financial markets, indirectly impacting the housing sector.

Regulatory Changes

Changes in housing policies, zoning laws, or lending regulations at federal, state, or local levels could also influence the market. For example, stricter lending standards could reduce the pool of eligible buyers, while more permissive zoning could boost supply. These regulatory shifts could significantly shape the dynamics of the 2026 Housing Market.

Conclusion: Navigating the 2026 Housing Market with Confidence

The 2026 Housing Market is poised to be a period of recalibration and opportunity. While the extreme volatility of recent years may subside, a nuanced understanding of economic indicators, mortgage rate forecasts, and regional specificities will be paramount. We anticipate a market characterized by moderating mortgage rates, persistent but easing supply constraints, and continued demand driven by demographic shifts.

For prospective homebuyers, 2026 could offer a more accessible entry point into homeownership, especially as rates stabilize and potentially dip. Patience and strategic planning, coupled with a keen eye on regional performance, will be key. For investors, the landscape will reward those who conduct thorough due diligence, identify underserved markets, and adopt flexible strategies. The Sun Belt is likely to remain a strong performer, while the Midwest offers stable, affordable options, and coastal markets will retain their long-term value, albeit with slower appreciation.

Ultimately, success in the 2026 Housing Market will hinge on staying informed, adapting to evolving conditions, and making data-driven decisions. By carefully monitoring the factors outlined in this analysis, individuals and investors alike can position themselves to thrive in the real estate environment of 2026 and beyond.