2026 Credit Score Changes: Your Comprehensive Guide to Financial Preparedness

Understanding the 2026 Credit Score Changes: What You Need to Know to Improve Your Financial Standing (RECENT UPDATES, PRACTICAL SOLUTIONS)

The world of personal finance is constantly evolving, and one of the most critical components of your financial health, your credit score, is no exception. As we approach 2026, significant shifts are on the horizon for how credit scores are calculated and utilized. These upcoming 2026 credit score changes are not just minor tweaks; they represent a fundamental re-evaluation of what constitutes creditworthiness. For consumers, lenders, and financial institutions alike, understanding these changes is paramount to navigating the future financial landscape successfully. This comprehensive guide will delve into the anticipated modifications, their potential impact, and, most importantly, provide you with actionable strategies to prepare and even improve your financial standing in light of these developments.

The Evolving Landscape of Credit Scoring: Why Changes Are Coming

Credit scores have become an indispensable part of modern financial life. From securing a mortgage or car loan to renting an apartment or even getting a cell phone plan, your credit score plays a pivotal role. For decades, the FICO score has been the dominant force, but other models like VantageScore have gained significant traction. The impending 2026 credit score changes are partly a response to several factors:

- Technological Advancements: With big data and advanced analytics, credit bureaus and scoring models are able to process and interpret a wider array of financial information than ever before.

- Demand for More Inclusive Scoring: There’s a growing recognition that traditional credit scoring models may not accurately assess the creditworthiness of all consumers, particularly those with thin credit files or non-traditional financial histories. The goal is often to expand access to credit for more individuals.

- Lender Needs: Lenders are always seeking more predictive and accurate tools to assess risk. Newer models aim to provide a more nuanced understanding of a borrower’s ability and willingness to repay.

- Regulatory Pressure and Consumer Advocacy: Calls for greater transparency, fairness, and accuracy in credit reporting have influenced the development of new scoring methodologies.

These forces are converging to reshape how your financial behavior is translated into a credit score, making it essential to understand the specific alterations that will define the 2026 credit score changes.

Key Anticipated 2026 Credit Score Changes and Their Implications

While the specifics are still being finalized and rolled out, several significant changes are expected to take effect by 2026. These changes primarily revolve around the inclusion of new data points, the re-weighting of existing factors, and the introduction of updated scoring models.

1. Increased Emphasis on Rent and Utility Payments

One of the most anticipated 2026 credit score changes is the broader inclusion of positive rent and utility payment history. Historically, these payments were rarely factored into traditional credit scores unless they went to collections. This meant that individuals who consistently paid their rent and utility bills on time received no credit benefit, while those who defaulted saw a significant negative impact.

- Impact: This change is particularly beneficial for consumers with limited credit history (often referred to as ‘thin files’) or those who primarily manage their finances through rent and utility payments rather than traditional credit products. It could help millions of Americans establish or improve their credit scores, potentially opening doors to better loan terms, housing opportunities, and more.

- Actionable Advice: If you consistently pay your rent and utilities on time, consider services that report these payments to credit bureaus (e.g., Experian Boost, Rental Kharma, LevelCredit). Ensure all your accounts are in good standing to maximize this positive impact.

2. Refined Treatment of Buy Now, Pay Later (BNPL) Services

The explosion of BNPL services has posed a challenge for traditional credit scoring models. Initially, many BNPL transactions were not reported to credit bureaus. However, as these services become more prevalent, the major credit bureaus are working to incorporate them into scoring models.

- Impact: The inclusion of BNPL data could be a double-edged sword. On-time payments could positively contribute to your credit history, especially for those with limited traditional credit. However, missed payments or excessive use of BNPL leading to overextension could negatively affect your score. The key will be how consistently and responsibly consumers use these services.

- Actionable Advice: Treat BNPL payments with the same seriousness as credit card payments. Make sure you can comfortably afford the installments. If you use BNPL, ensure the provider reports positive payment history to the credit bureaus.

3. Enhanced Focus on Cash Flow Data and Banking Transaction History

Some newer scoring models are exploring the use of banking transaction data, including checking and savings account activity, to assess creditworthiness. This could include analyzing consistent income, savings patterns, and the absence of overdrafts.

- Impact: This is a more profound shift, moving beyond traditional credit accounts to a more holistic view of financial behavior. It could benefit individuals who manage their bank accounts responsibly but may not extensively use credit cards or loans. It also provides lenders with a richer, more real-time snapshot of financial stability.

- Actionable Advice: Maintain healthy banking habits. Avoid frequent overdrafts, keep a stable balance, and demonstrate consistent income. While this data is typically only used with your explicit consent, understanding its potential influence is important.

4. Changes to How Medical Debt is Handled

Medical debt has long been a contentious issue in credit reporting. Recent changes have already removed paid medical collections from credit reports, and unpaid medical collections under a certain threshold ($500) are also being excluded. Further refinements are expected by 2026.

- Impact: These changes are overwhelmingly positive for consumers, preventing medical emergencies from disproportionately damaging credit scores. It recognizes that medical debt often arises from unforeseen circumstances rather than irresponsible financial behavior.

- Actionable Advice: Continue to monitor your credit report for any inaccuracies related to medical debt. If you have outstanding medical bills, try to negotiate with providers or insurers to prevent them from going to collections, or to settle them quickly if they do.

5. The Rise of Alternative Data and Advanced Analytics

Beyond the specific data points, the underlying algorithms used by credit scoring models are becoming more sophisticated. This includes leveraging artificial intelligence and machine learning to identify patterns and predict risk more accurately.

- Impact: This could lead to more personalized and precise credit assessments. While beneficial for accuracy, it also means that a wider range of your financial activities could indirectly influence your score, even if not directly reported as a credit account.

- Actionable Advice: Focus on overall financial wellness. Every financial decision, from how you manage your bank accounts to how you pay your bills, contributes to your financial footprint.

Understanding the Different Credit Scoring Models: FICO vs. VantageScore

It’s crucial to remember that there isn’t just one credit score. The 2026 credit score changes will impact different models in varying ways. The two most prominent scoring models are FICO and VantageScore.

FICO Scores

FICO (Fair Isaac Corporation) has been the industry standard for decades. There are multiple versions of FICO scores, with FICO 8 being widely used, and FICO 9 and FICO 10 T (which incorporates trended data) gaining traction. FICO scores typically range from 300 to 850.

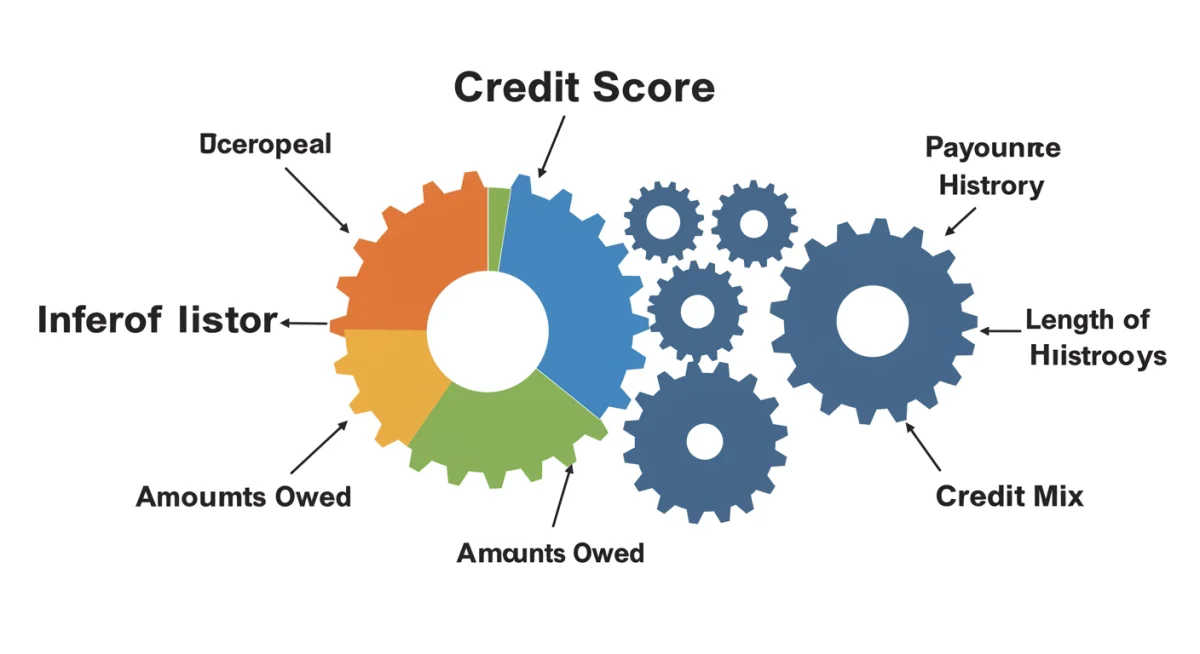

- Key Factors: Payment history (35%), amounts owed (30%), length of credit history (15%), new credit (10%), and credit mix (10%).

- Likely 2026 Changes: FICO has already introduced models like FICO 9 and FICO 10 T that are more forgiving of medical collections and incorporate trended data (how balances change over time). Future iterations will likely continue to integrate alternative data sources where permitted and proven predictive.

VantageScore

VantageScore is a newer model developed by the three major credit bureaus (Experian, Equifax, and TransUnion) as a competitor to FICO. VantageScore 3.0 is commonly used, and VantageScore 4.0 is designed to be more inclusive.

- Key Factors: Total credit usage, balance, and available credit (extremely influential); credit mix and experience (highly influential); payment history (moderately influential); age of credit history (less influential); new credit (less influential).

- Likely 2026 Changes: VantageScore 4.0 already places a strong emphasis on trended data and is designed to score more consumers, including those with thin files. It also treats paid collections more favorably. The 2026 credit score changes will likely see VantageScore continue to lead the way in incorporating non-traditional data and advanced analytics to provide a more comprehensive view of creditworthiness.

It’s important to understand that lenders may use different versions of FICO or VantageScore, or even their own proprietary scoring models. The general trend, however, is towards more inclusive and predictive models that consider a broader range of financial behaviors.

Practical Solutions and Strategies to Prepare for 2026

Given these impending 2026 credit score changes, proactive steps are essential. Here’s how you can prepare and ensure your credit remains strong, or even improves:

1. Monitor Your Credit Reports Regularly

This is foundational. You are entitled to a free credit report from each of the three major bureaus (Experian, Equifax, and TransUnion) annually via AnnualCreditReport.com. Review them for accuracy, identify any discrepancies, and understand what information is being reported.

- Action: Dispute any errors immediately. Incorrect information can drag down your score.

2. Prioritize On-Time Payments

Payment history remains the single most important factor in both FICO and VantageScore models. Late payments, especially those 30, 60, or 90+ days past due, can severely damage your score.

- Action: Set up automatic payments for all your bills. Use calendar reminders. Never miss a payment due date for credit cards, loans, or even rent and utilities if they are being reported.

3. Keep Credit Utilization Low

Credit utilization refers to the amount of credit you’re using compared to your total available credit. High utilization indicates higher risk. Aim to keep your utilization below 30% on all revolving accounts, and ideally even lower (under 10%) for an excellent score.

- Action: Pay down credit card balances. If you have multiple cards, spread your balances to avoid maxing out any single card. Consider requesting a credit limit increase (if you won’t be tempted to spend more) to lower your utilization ratio.

4. Be Mindful of New Credit Applications

Each time you apply for new credit, a hard inquiry appears on your credit report, which can slightly ding your score. Opening too many new accounts in a short period can also signal risk.

- Action: Only apply for credit when absolutely necessary. Space out applications if you need multiple new accounts (e.g., a mortgage and a car loan).

5. Diversify Your Credit Mix (Responsibly)

Having a mix of different types of credit (e.g., installment loans like mortgages or car loans, and revolving credit like credit cards) can positively impact your score, showing you can manage various credit types.

- Action: If you only have credit cards, consider a small, secured loan if you need to build credit. However, never take on debt you don’t need or can’t afford just to diversify your credit mix.

6. Incorporate Positive Rent and Utility Payments

As mentioned, this will be increasingly important with the 2026 credit score changes.

- Action: Explore services like Experian Boost or similar platforms that allow you to link your bank accounts to report on-time rent and utility payments. Discuss with your landlord if they report payments to credit bureaus.

7. Manage Buy Now, Pay Later (BNPL) Usage Prudently

With BNPL data becoming more prevalent, responsible use is key.

- Action: Ensure you make all BNPL payments on time. Avoid over-committing to multiple BNPL plans that could strain your budget.

8. Maintain Healthy Banking Habits

If cash flow data becomes more integrated, your banking behavior will be more scrutinized.

- Action: Avoid frequent overdrafts. Maintain a consistent positive balance in your checking and savings accounts. Demonstrate responsible money management through your banking activities.

9. Address Any Outstanding Debts

While some medical debt reporting is changing, other forms of collections or past-due accounts will still significantly impact your score.

- Action: Create a plan to pay down or settle any outstanding collections or charge-offs. Even old negative marks can continue to impact your score.

Who Will Be Most Affected by the 2026 Credit Score Changes?

While everyone with a credit score will likely see some impact, certain groups may experience more significant shifts:

- Credit Invisibles/Thin Files: Individuals with little to no traditional credit history stand to benefit significantly from the inclusion of rent, utility, and BNPL payment data. These changes could finally give them a pathway to establishing credit.

- Responsible Renters: Those who consistently pay rent on time but don’t own homes or extensively use credit cards will see their financial diligence recognized.

- BNPL Users: Responsible users will see a positive impact, while those who struggle with BNPL payments could see a negative effect.

- Consumers with Medical Debt: These individuals will likely see an improvement in their scores due to more lenient treatment of medical collections.

- Lenders: Lenders will gain a more comprehensive view of borrower risk, potentially leading to more accurate lending decisions and expanded access to credit for a wider pool of applicants.

The Long-Term Outlook: What Does This Mean for Your Financial Future?

The 2026 credit score changes reflect a broader trend towards more sophisticated, inclusive, and dynamic credit assessment. The goal is to create a more equitable system that better reflects an individual’s true financial behavior rather than relying solely on traditional credit products. For consumers, this means that every financial habit, from paying your phone bill to managing your checking account, could potentially contribute to your overall financial reputation.

This evolution underscores the importance of holistic financial management. It’s no longer just about paying your credit card on time; it’s about demonstrating consistent financial responsibility across all facets of your financial life. Adopting good financial habits now will not only prepare you for the 2026 credit score changes but will also lay a strong foundation for long-term financial stability and success.

Conclusion: Take Control of Your Credit Future

The upcoming 2026 credit score changes represent a significant evolution in how creditworthiness is assessed. By understanding these shifts, monitoring your credit reports, and adopting proactive financial strategies, you can not only mitigate any potential negative impacts but also leverage these changes to your advantage. Whether it’s ensuring your rent payments are reported, managing your BNPL accounts responsibly, or simply maintaining excellent banking habits, taking control of your financial data is key. Your credit score is a reflection of your financial health, and with these changes, it’s becoming an even more comprehensive one. Start preparing today to secure a stronger financial future.

Frequently Asked Questions About 2026 Credit Score Changes

- Q: When exactly will the 2026 credit score changes take effect?

- A: While the term ‘2026’ is used as a general timeline, some changes are already being phased in, and others will continue to roll out over the next few years. It’s an ongoing evolution rather than a single, sudden switch. Staying informed through reputable financial news sources is advisable.

- Q: Will these changes make it harder or easier to get credit?

- A: For many, especially those with thin credit files or responsible payment histories for rent and utilities, it could make it easier to establish or improve credit. For others who are less financially disciplined, particularly with new data points like BNPL, it could highlight areas for improvement. Overall, the aim is to provide a more accurate and inclusive assessment, which should benefit a broader range of responsible consumers.

- Q: Do I need to do anything specific to have my rent or utility payments reported?

- A: Yes. Currently, most landlords and utility companies do not automatically report positive payment history to all three major credit bureaus. You typically need to opt into a third-party service (like Experian Boost, Rental Kharma, or LevelCredit) that collects and reports this data on your behalf. There might be a fee associated with these services.

- Q: How can I check which credit score model my lender uses?

- A: It’s often difficult to know precisely which version of a FICO or VantageScore model a specific lender will use, as they can vary by loan product and lender. However, focusing on the fundamental principles of good credit management (on-time payments, low utilization, diverse credit mix) will positively impact all major scoring models, regardless of the version.

- Q: Are there any negative impacts of these 2026 credit score changes?

- A: The primary ‘negative’ impact would be for individuals who are not managing alternative forms of credit (like BNPL) or their banking accounts responsibly. If these behaviors are now factored in and show irresponsibility, it could potentially lower a score that previously wasn’t affected by these specific actions. The key is consistent, responsible financial behavior across the board.